Market correction in alt protein?

Also: how inflation and supply chain issues are affecting alt protein in APAC

Part 1

Food prices inflation and supply chain issues are all over the headlines – driven by the pandemic and more recently the war in Ukraine and the global economic downturn.

But how is the alt protein sector is affected?

I asked a bunch of APAC startup founders. These are sensitive topics, so most folks requested not to be named. Still, the quotes and insights are all real.

Michael Fox, a co-founder of Fable, an Aussie mushroom-based meat startup, says their supply chain “has been relatively unimpacted”.

The biggest issue for Fable has been shipping – the costs are higher and it takes much longer. Other founders concur:

“We had to increase inventory levels due to ongoing freight delays.”

“Shipments coming out of China have been severely delayed. Rates remain elevated and facing constant delays.”

What about ingredients’ cost and availability? While no one I talked to had to reformulate their products yet, many experienced disruptions.

A plant-based meat startup in India replaced protein ingredients from China with locally sourced ones. The price of wheat fibre they are getting from Poland increased by 49% since last year.

CEO of a very well-funded APAC plant-based meat company told me:

“Our team has worked hard to qualify alternative raw materials when original sources were unavailable”

Startups working with cell-based and precision fermentation tech also had their challenges. They focus on R&D and noticed increased wait times for equipment and materials. Mihir Pershad, founder of cultivated fish startup Umami Meats said:

“Equipment lead times are now 5-7 months when they used to be 2-3, and generally much less reliable now.”

The cost of lab materials/consumables has gone up by 10-20%, according to several founders.

It’s a bit different in China – one biotech founder only saw “minimal impact” since they are sourcing their consumables locally. But they had to switch to bioreactors produced in China, as importing would take too long.

Back to plant-based founders, have they had to adjust prices?

A founder of a leading plant-based milk startup in Asia told me:

“No, we have not. Though we have been subject to some inflation, we are absorbing it.”

Seems like that is a typical approach. Another company shared that their gross margin is down 2-3% as they absorbed the highest cost of shipping and ingredients.

The Indian startup previously mentioned also took it in but “may have to increase [prices] if the situation continues”.

Some already did. The CEO of the same very well-funded APAC startup:

“We had to increase some pricing to reflect the high levels of inflation but have kept these to a minimum and are now much closer to our aim of price parity against meat.”

And since animal products are now also getting more expensive, can the holy grail of “price parity” be finally within reach? It could be the one silver lining in the inflation/supply chain story so far.

There are already a few signs it is happening, at least in Europe/the US.

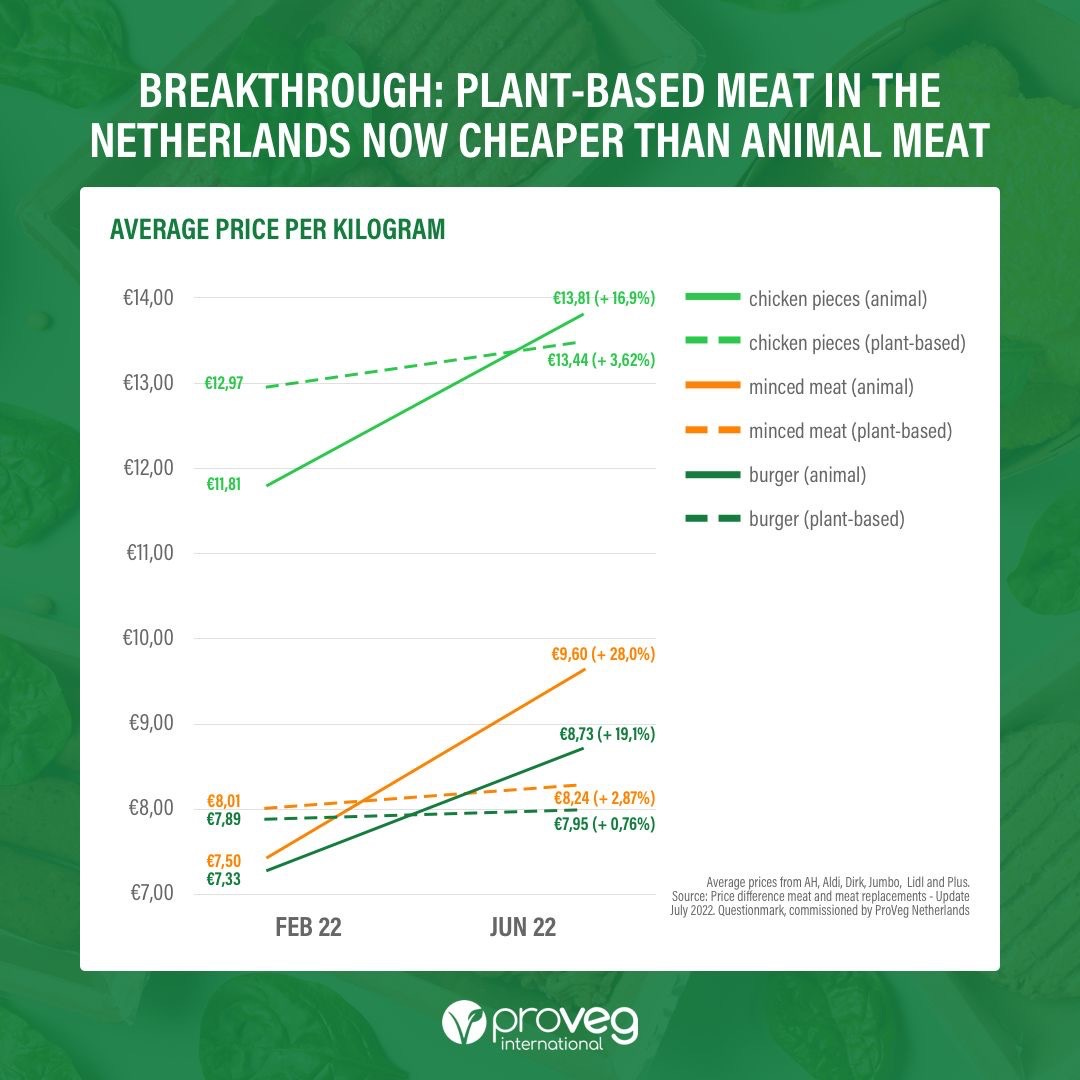

According to an analysis by ProVeg International, in the Netherlands some plant-based meat products are now slightly cheaper than animal-based (a quick check via the online store of NL’s largest supermarket Albert Heijn mostly confirmed the data):

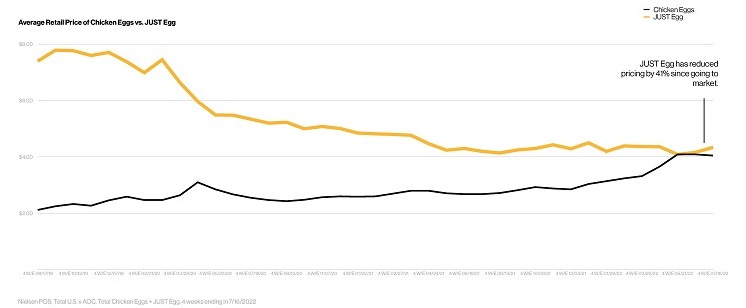

Another example comes from the US. In a recent interview by FoodNavigator, a plant-based egg startup Eat Just said they have reached price parity with “premium eggs”. They shared this chart, showing the gap is closing, driven more recently by the fast-increasing retail price of chicken eggs:

In the few weeks since the data has been collected, the retail price of eggs has fallen considerably in the US, according to Bloomberg. At the time I write this in late August, Just Egg is the most expensive option at Walmart with ~$0.49/egg equivalent. It’s slightly more than premium organic eggs and >50% more than regular cage-free eggs.

That shows some of these gains might be temporary and the price ratio will change as the global supply chain issues ease. We have seen it here in Asia with pork prices. They shot up dramatically last year due to ASF and then went back down as the outbreak got under control.

But the price of animal products tends to be more volatile (to prove the point, China’s pork prices are rising again) . Pablo Moleman of ProVeg Netherlands explains it well:

“Meat has always been a product that requires an enormous amount of raw materials. To make one kilogram of meat, you need up to ten kilograms of grain. Now, in times of scarcity, that takes its toll […] Plant-based meat clearly wins out on efficiency, and we now see that reflected in the price.”

My take: much more to be done, but the industry is on a good track when it comes to price parity.

With all of these supply chain and inflation challenges, what are APAC founders saying about the near future?

Here are several takes:

“We expect supply disruptions to continue in ways that are hard to predict!”

“China should open up towards year-end, relieving some supply chain issues. The freight issue seems a little more structural and could take longer to resolve. Expecting continued inflation next 2 years.”

“In addition to the war in Ukraine, we now have tension in the Taiwan strait between the US and China. This could be even more destabilising than the war in Ukraine and COVID combined.”

And for some, it strengthens their conviction in alt protein as a solution due to a more sustainable supply chain. From Michael Fox of Fable:

“We can’t control geopolitics, but we aim to build a flexible, adaptable, anti-fragile supply chain so that we can take advantage of major disruptions which usually harm large, fragile incumbents, like the meat industry, more than they harm us.”

Another CEO:

“Whilst this is challenging for many businesses, including our own, it also reinforces the urgency of our mission to provide a new version of food and relieve the huge pressure on our planet’s resources.”

Part 2

How is the funding environment shifting?

Public tech companies are trading 60-70% below pre-pandemic prices.

Plant-based startups on NASDAQ have not been spared: Oatly lost over 80% of value since its IPO last year and Beyond Meat over 70% compared to early 2020. In both cases, the stock price drop is amplified by their own supply chain and manufacturing struggles.

No surprise that in this environment almost all new IPOs are being postponed.

At the same time, VCs are channelling less money to startups – across all sectors, Q2 is down 27% YoY and 26% QoQ.

Alt protein funding globally is also down, but not as much so far: -9% in Q2 to $833 million.

Q2 numbers are boosted by a large $400m Series C of Upside Foods in the US.

With $1.7b total invested in alt protein during the first half of the year, 2022 is on track to be well below the record $5b mark from last year.

I talked to several investors focused on this sector to get their take.

Gautam Godhwani, a managing partner of Singapore-based VC Good Startup, investing in alt protein startups globally said:

“The alternative protein industry has not been immune to the economic downturn. Rounds are taking longer to close, at a smaller size, and with lower valuations.”

Yiren Chen, managing director at Genedant, a life science and alt protein investor based in Singapore believes that “the correction affected many late-stage, high-growth yet unprofitable companies.”

Indeed, from what I see and hear, pre-seed and seed stages are relatively less affected, and the impact is most visible in later-stage funding.

Valuations are dropping, in some cases significantly. The most tricky are sizeable Series B/C – finding a strong lead is often harder now. Many startups at that stage are postponing the raise, choosing to go for smaller bridge rounds, and relying on existing investors more. Expensive projects like pilot plants are being scaled down or delayed. I expect a hiring freeze and even layoffs for some of those more mature startups.

Let’s zoom into Asia Pacific:

The numbers for APAC are looking good so far. My best estimate for the region’s alt protein funding in 2022 up till now is $400-450m. That already beats est. $312m raised by region’s startups in full 2021. We are heading for a new record, likely exceeding $500m.

The figure includes several large Series A/B in the region raised this year:

- Next Gen Foods (TiNDLE), Singapore – $100m Series A in January

- Starfield, China – $100m Series B in January

- Oatside, SG/Indonesia – $65.6m Series A in July

- Armored Fresh (Yangyoo), Korea – $23m Pre-Series B in May

- Changing Biotech, China – $22m Series A in June

Despite these encouraging numbers, a mood shift is visible here in APAC as well.

A founder of a TOP3 best-funded startup in the region told me:

“We are being advised that it is not a good time to raise at the moment. It’s a good time to have a long runway!”

Michael Fox of Fable has been open about his recent experience with fundraising:

“The funding environment shifted in the middle of us raising our Series A and we certainly felt investor sentiment shift.”

Has Michael managed to close the round and what helped?

“We’ve taken a product lead approach with healthy gross margins. We had some P&L profitable months in late 2021. We’ve found a strong product market fit. This served us well and we’re now closing our Series A with some great new investors joining, and existing investors coming in again.”

This focus on ‘fundamentals’ like gross margins and the product-market fit is mentioned often in my conversations. Albert Tseng, co-founder of Dao Foods, an alt protein incubator focusing primarily on China startups:

“Given the global market downturn, we definitely see VC investors become increasingly cautious in alternative protein both globally and in China. In tight markets, investors tend to move back to fundamentals.”

Matilda Ho, a managing director of China’s agri-food tech VC Bits x Bites also talks about fundamentals – but from a consumer expectations angle:

“Investors are becoming more selective and rightfully so. We believe the opportunity remains strong for companies that can fundamentally elevate the taste and quality of the entire product category.”

And how are APAC investors adjusting their approach to investing in this new reality?

Yiren of Genedant told me:

“For early stage companies, we nudge the founders more towards commercialisation and suggest to be more cost conscious. Great ideas need to be paired with strong operational foundations.”

Dalal AlGhawas, the program director for Big Idea Ventures alt protein accelerator in Singapore said:

“At BIV we are focusing more on scalability. We are assessing ingredients and production solutions that provide affordable and practical means to integrate into existing food supply chains.”

She is also happy to see “more start-ups in APAC regions starting to look into fermentation and cell cultivation”, given the friendly “regulatory framework in Asia to embrace these novel foods” – pointing out the recent Singapore launch of Coolhaus/Perfect Day ice cream product made with precision fermentation whey.

Gautam of Good Startup takes a “two-pronged approach”:

“First, we are working with our portfolio companies to ensure they have at least 18 months of runway. Second, we are finding investments where teams are taking a long term view to emerge from the economic downturn with a viable product and market development strategy.”

Not surprisingly, “long-term” is a common phrase these days. Albert of Dao Foods is looking for founders with “strong product orientation, who have the passion to stay in for the long term.”

Speaking of the long-term, APAC investors remain positive about the future of the sector, with a few caveats:

Matilda of Bits x Bites said:

“The best companies that have strong technology and can bring a great product at scale and at competitive costs will continue to be sought after.”

Gautam of Good Startup added:

“Despite a short term dip, the alternative protein sector will continue to grow. APAC will become the largest market for alternative proteins within the next few years, so the region will see accelerating investment levels.”

Albert of Dao Foods highlighted the impact aspect:

“Climate change continues to accelerate, so it is at this time that impact investors can be especially catalytic by providing growth capital, especially in under-invested geographies such as China.”

And Yiren of Genedant told me:

“Alternative protein is here to stay and will be a major part of food production in future. The question is how quickly it will be mainstream, especially in developing economies where the protein need is highest.”

I tend to agree with these sentiments. However, my day job is investing in alt protein startups in Asia Pacific (via Better Bite Ventures), so I am rather biased 😊

Yes, the bar for successful startups in the region is even higher now and the timeline for ‘mainstreaming’ alt protein in Asia might not be 100% clear.

But the core drivers remain intact: more and more consumers follow a flexitarian diet, reducing their animal product consumption, while alt protein can also be one of the solutions to the climate crisis.

Finally, I cannot overstate the importance of the APAC region. Yes, I am biased (did I mention it already?), but the numbers do not lie: it is the world’s largest protein market with over 40% of global meat and over 70% of seafood consumption. Still, less than 20% of dollars invested in the alt protein sector goes to APAC startups.

Closing this funding gap will need to happen for a successful and truly global transition towards a more sustainable protein system.